201

Personal Finance

4684 readers

8 users here now

Learn about budgeting, saving, getting out of debt, credit, investing, and retirement planning. Join our community, read the PF Wiki, and get on top of your finances!

Note: This community is not region centric, so if you are posting anything specific to a certain region, kindly specify that in the title (something like [USA], [EU], [AUS] etc.)

founded 2 years ago

MODERATORS

202

203

204

205

206

16

[Daily discussion] How do you deal with relatives or friends making bad financial decisions?

(discuss.tchncs.de)

207

208

209

210

211

18

for a savings account that calculates interest daily and pays interest monthly, is it better to contribute daily or monthly?

(lemmy.world)

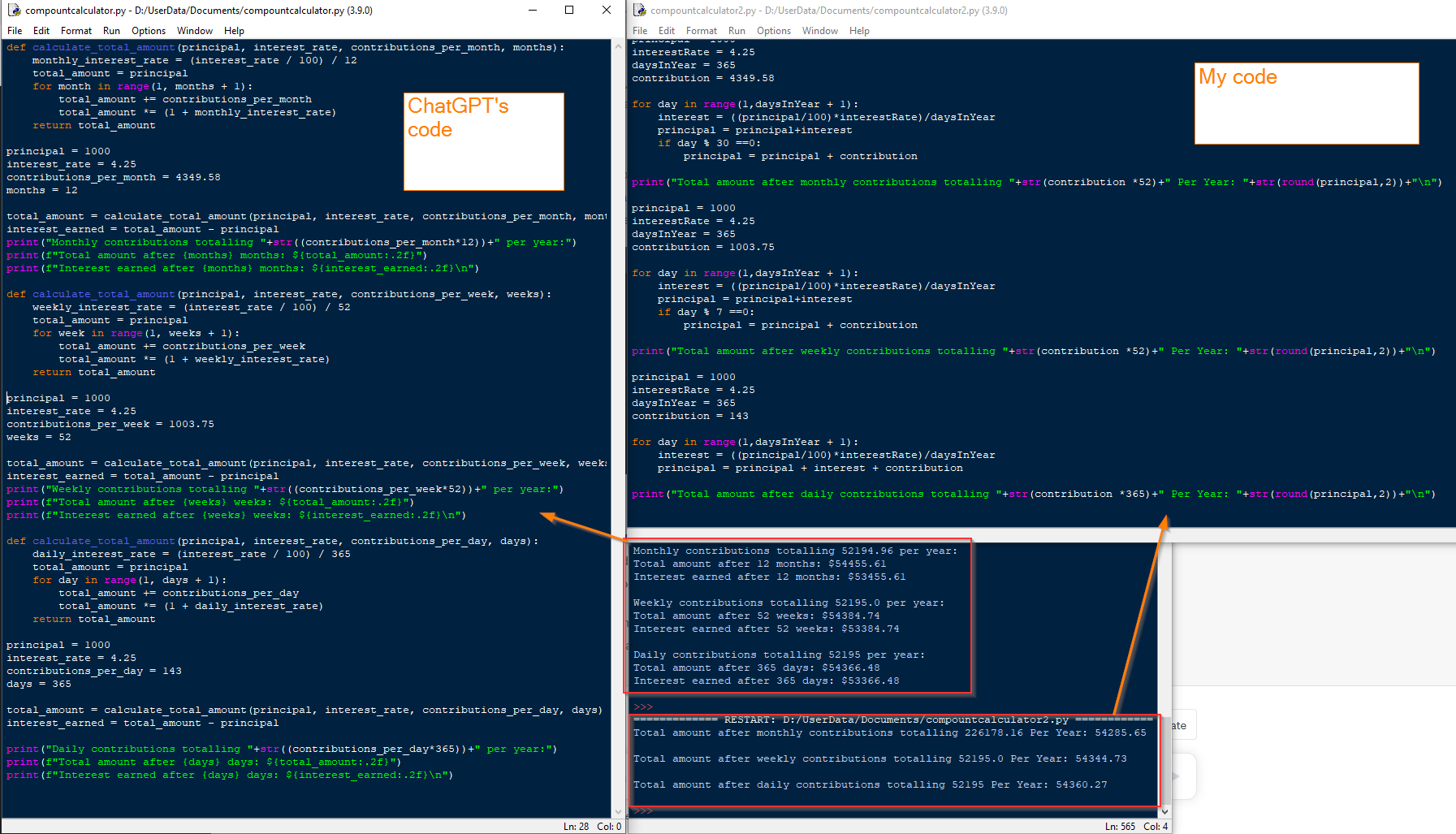

So i got into a disagreement with ChatGPT about whether you earn more interest overall if you contribute daily rather than monthly, if the overall contribution over 1 year is the same.

I made CGPT write some python code to prove it. His code is on the left. I still didnt believe him so I wrote my own, on the right.

Our results seem to disagree, so Im asking you guys, if your interest is calculated daily and paid monthly, is it better to contribute $143 per day for 365 days, or $4349.58 monthly for 12 months?

212

213

16

AI will be at the center of the next financial crisis, SEC chief Gary Gensler says

(markets.businessinsider.com)

214

215

216

217

218

219

220

221

222

223

224

225