126

Personal Finance

4678 readers

29 users here now

Learn about budgeting, saving, getting out of debt, credit, investing, and retirement planning. Join our community, read the PF Wiki, and get on top of your finances!

Note: This community is not region centric, so if you are posting anything specific to a certain region, kindly specify that in the title (something like [USA], [EU], [AUS] etc.)

founded 2 years ago

MODERATORS

127

128

129

130

131

132

91

Mint.com is going away. Are there any alternatives that are as automatic and simple?

(www.theverge.com)

133

134

135

136

137

138

cross-posted from: https://sh.itjust.works/post/7528778

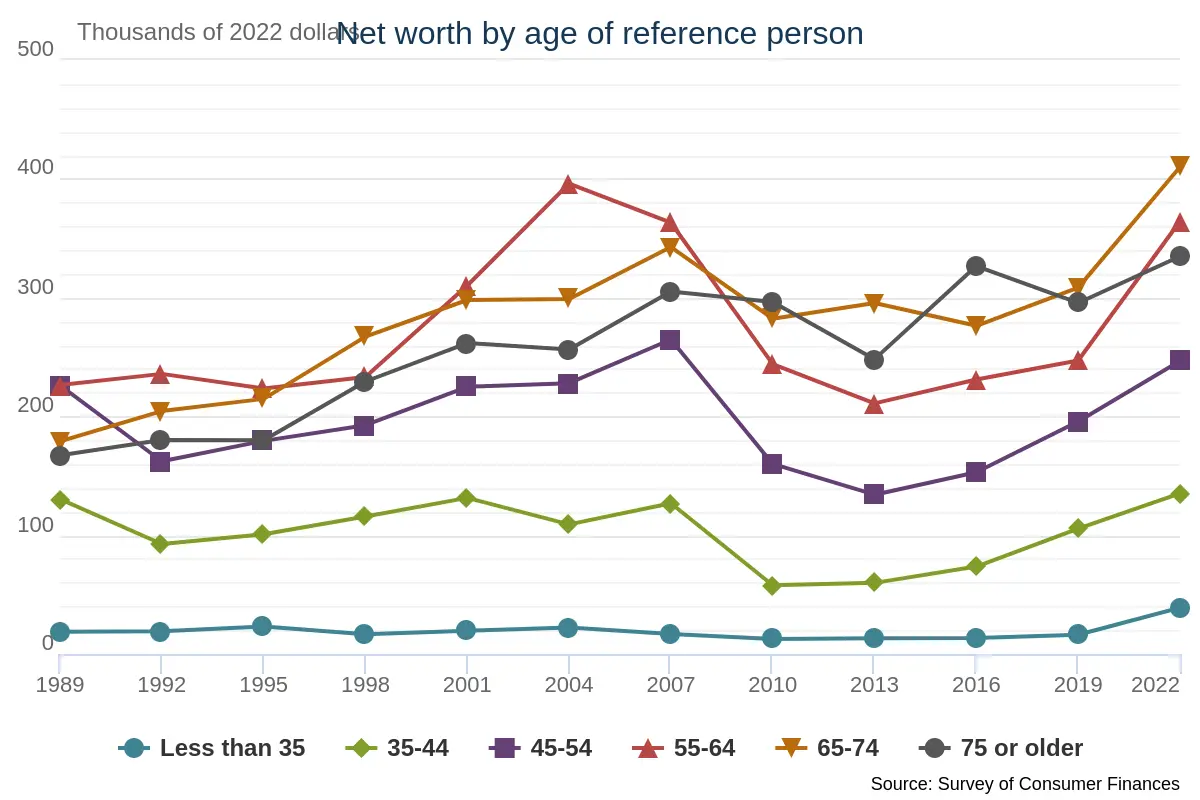

Age 2022 Net Worth (Median) USD$ Less than 35 $39,040 35-44 $135,300 45-54 $246,700 55-64 $364,267 65-74 $410,000 75 or older $334,700 Source:

https://www.federalreserve.gov/econres/scf/dataviz/scf/chart/

139

{kind=link}

141

142

143

144

145

146

147

148

149

150