1366

you are viewing a single comment's thread

view the rest of the comments

view the rest of the comments

this post was submitted on 26 Nov 2023

1366 points (94.5% liked)

A Boring Dystopia

9741 readers

1146 users here now

Pictures, Videos, Articles showing just how boring it is to live in a dystopic society, or with signs of a dystopic society.

Rules (Subject to Change)

--Be a Decent Human Being

--Posting news articles: include the source name and exact title from article in your post title

--Posts must have something to do with the topic

--Zero tolerance for Racism/Sexism/Ableism/etc.

--No NSFW content

--Abide by the rules of lemmy.world

founded 1 year ago

MODERATORS

It was supposed to be a three-pronged plan: Social Security, 401k, and corporate pension. Each of these has problems on their own, but a hybrid solution could cover for each other's issues.

Now, corporate pensions are rare, 401k's are highly vulnerable to stock market crashes, and Social Security is being slowly strangled.

not really. short term investments and speculation are vulnerable to short term market forces, but a 401k that sits for 30 years with regular contributions and profits reinvested is all but guaranteed to make money. Long term investments like that are extremely stable, just put the money in your 401k and don't look at returns until you're actually considering retirement.

What's critical is where the stock market is at when you retire. Stock market crashes coming with general economic problems mean older people lose their jobs, can't find another one, and are forced to retire with 40% of their 401k value knocked out. This is exactly what happened to people in 2008 and '09.

Conversely, the stock market did really well in the years after that. The people who were able to hold out past 2012 were able to get a nice nest egg saved up.

It's a dice roll. It can work as one part of a larger system, but not on its own.

40% of the value before the crash, I assume? In that case, what's the difference between their contributions and the total value even with that 40% gone? Remember that the real value of an investment is how much money is there now vs how much you put in, not how much money is there at peak value vs how much money is there now.

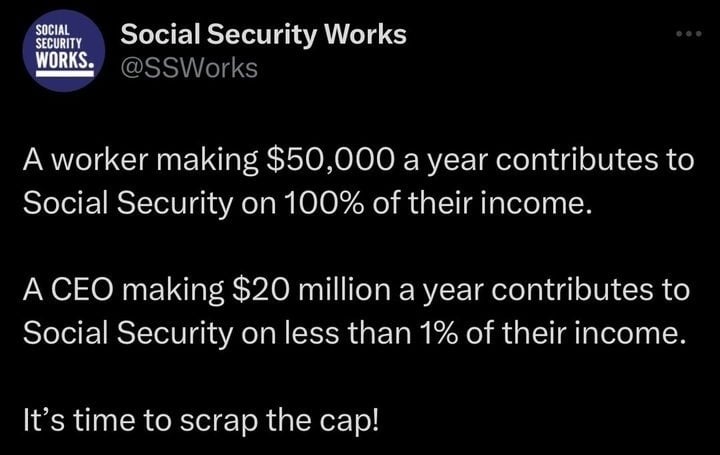

The demographics are probably a bigger part of it. The ratio of people collecting to people paying in is much larger now and the length of time people collect on it is longer since people live longer now.

Most corporate pension for workers are a joke. All the money goes to the top few.

No problem, just make a self-directed IRA that buys bitcoin. Immune to stock market crashes!