101

16

[US] Dual Income Life Insurance Question

(lemmy.world)

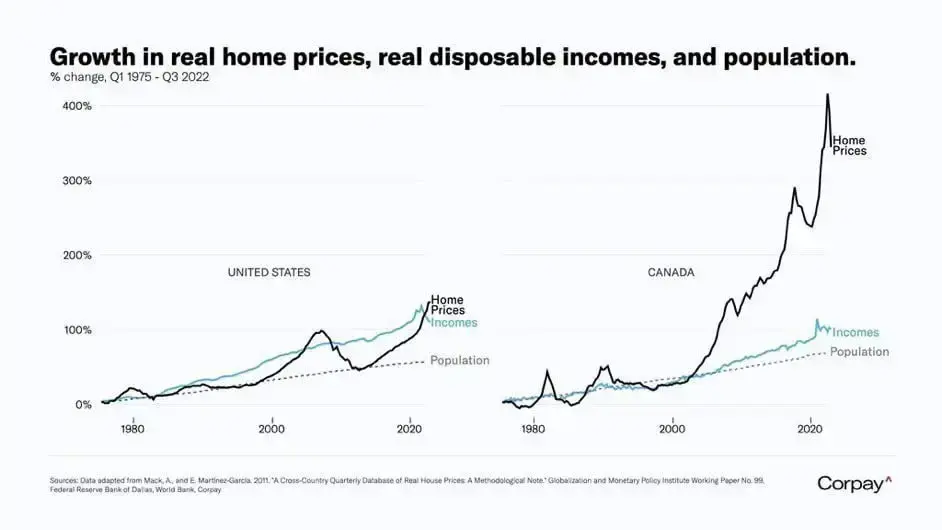

Definitely a trend I see around me (Europe, 30 years old).

All of my friends able to buy got at least 30k - 50k from their parents.

Is it the same around you? How do you deal with this?

Also, some data from a few days back:

https://discuss.tchncs.de/post/2426785?scrollToComments=true

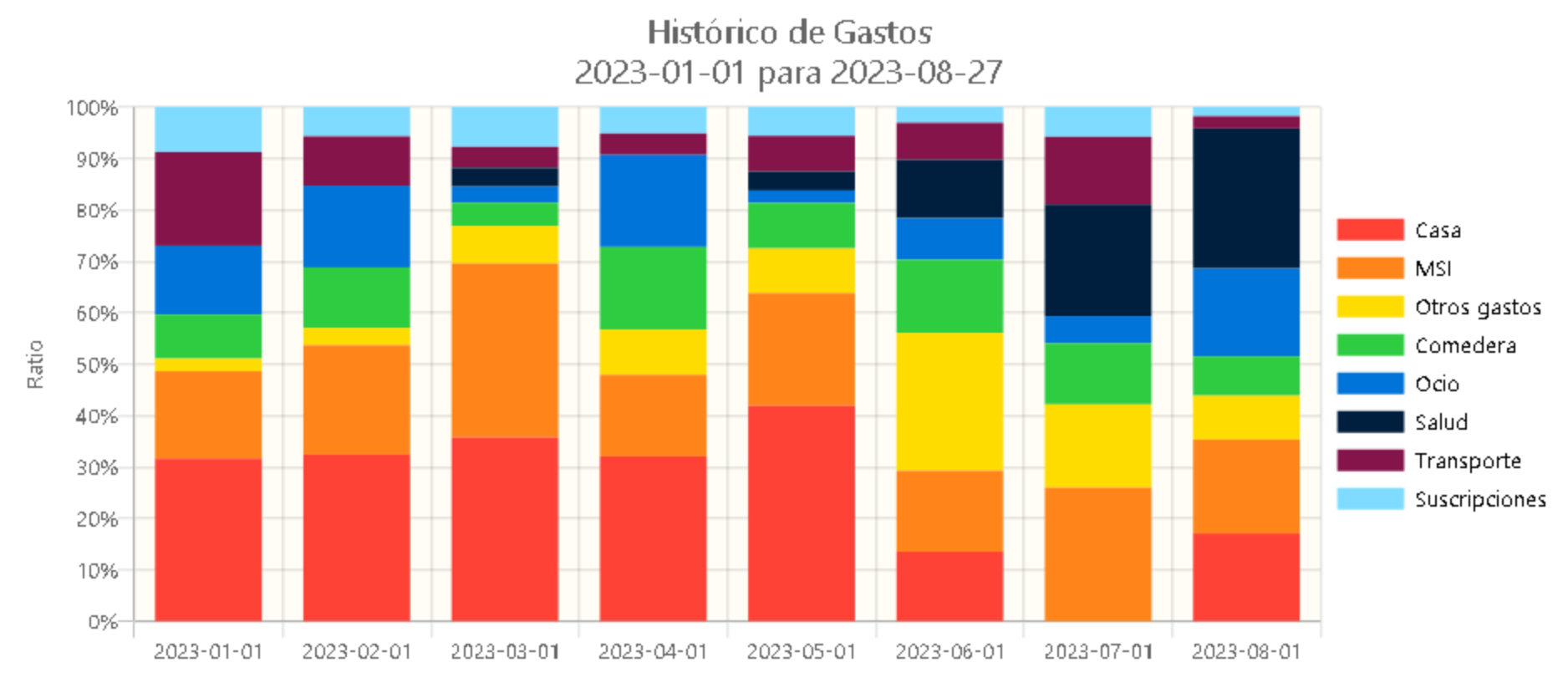

At the end of 2022, I discovered this software that I've been using all year. I'd like to hear your thoughts or experiences with GnuCash, or whatever system/program you use to track your personal finances!

For the ones unfamiliar, it's based on a double-entry accounting system; every transaction always has at least two accounts involved. Example: if I spend 200 SEK on a restaurant, it goes from Assets:Cash to Expenses:Food.

Starting by creating my own accounts, it helped me immensely to have an overview of my general financial situation.

Around March, I found enlightening to re-define what expenses needed their own category from what I was unconsciously lumping into 'others'. Having it all already logged, made it quite easy . The caveat is that all the entries are manual, but my finances are not as complex, so with 30-45 minutes a week I have it updated.

You can even create diagrams for your monthly expenses, or general balance, among other reports that come quite handy if you want to run a query.

Learn about budgeting, saving, getting out of debt, credit, investing, and retirement planning. Join our community, read the PF Wiki, and get on top of your finances!

Note: This community is not region centric, so if you are posting anything specific to a certain region, kindly specify that in the title (something like [USA], [EU], [AUS] etc.)